![]()

Advertiser Disclosure

Last update: June 11, 2025

9 minutes read

Can FAFSA Cover Graduate School Expenses? (The Truth)

Learn how FAFSA can fund your master’s degree and unlock state grants, employer tuition benefits, and tax deductions to reduce out-of-pocket costs for graduate school.

By Brian Flaherty, B.A. Economics

Edited by Rachel Lauren, B.A. in Business and Political Economy

Learn more about our editorial standards

By Brian Flaherty, B.A. Economics

Edited by Rachel Lauren, B.A. in Business and Political Economy

Learn more about our editorial standards

While the FAFSA remains your primary gateway to federal aid, savvy grad students know that state- and institution-based grants, employer tuition support, and tax breaks can dramatically lower out-of-pocket costs.

If you’re wondering "Can you get FAFSA for graduate school?", the answer is a resounding yes—as long as you understand how FAFSA for graduate school works, when to apply, and which programs go beyond the basics.

Whether you’re searching for FAFSA for grad school or trying to figure out "Does FAFSA pay for graduate school?", this guide will show you the top three funding pathways to minimize debt.

Key takeaways

- FAFSA covers graduate school, with the application process being similar for both undergraduates and graduates

- Graduate financial aid differs from undergraduate aid, with grads being considered independent and responsible for higher loan interest rates

- Graduate students are eligible for Direct Unsubsidized Loans and Direct PLUS Loans but not Pell Grants

Can FAFSA cover graduate school?

Yes, FAFSA covers financial aid for graduate school. The process is similar to the one undergraduates go through, with the main difference being the kind of aid and loans available to grad students.

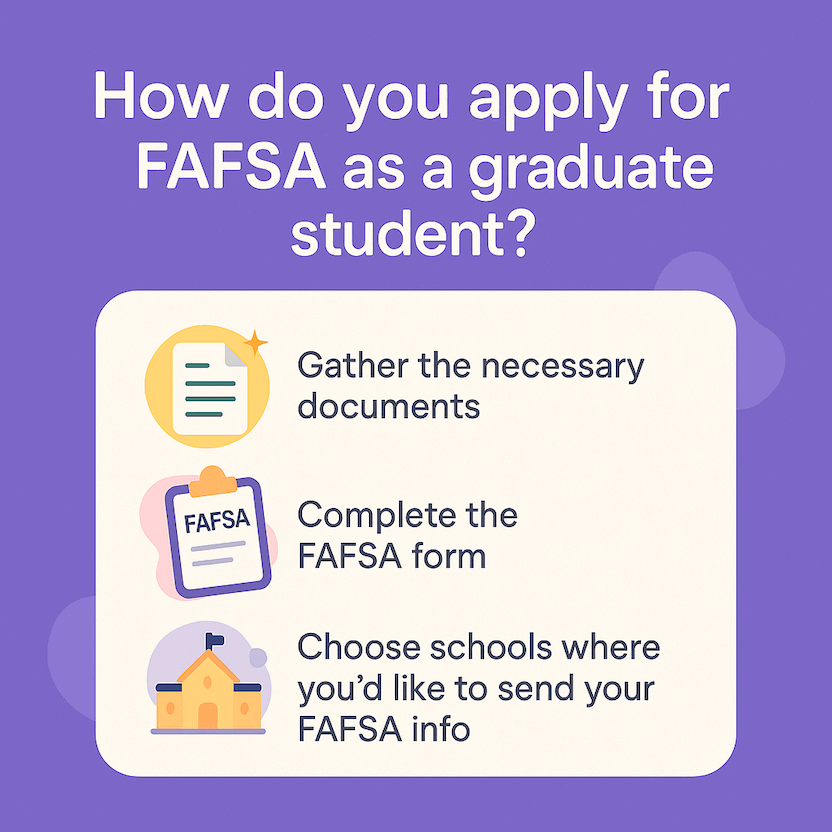

How do you apply for FAFSA as a graduate student?

Just like undergraduate students, graduate students fill out the FAFSA to help secure their financial aid. It's a straightforward process:

- Gather the necessary documents, including tax returns and bank account information.

- Set aside approximately 30 minutes to complete the FAFSA form.

- Choose up to 10 schools where you'd like to send your FAFSA information.

How does graduate financial aid differ from undergraduate aid?

Financial aid administrators consider grad students independent from their parents. That means whether you're living with mom and dad or on your own, your parents' financials don't factor into your FAFSA form.

Interest rates are also different between grad and undergrad studies. Graduate loans carry a 7.05% rate for federal direct unsubsidized loans (2023-2024), while undergrad loans are at a cooler 5.50%.

Unfortunately, Pell Grants, a type of gift aid, are off-limits to grad students. However, post-baccalaureate teacher certification students may still qualify.

But hey, there's good news too! Grad students can apply for grants like:

- Federal Fulbright Grants

- Certain grants offered by private organizations

- Teacher Education Assistance for College and Higher Education (TEACH) Grant

When I was paying my way through school, I tried to use grants as much as possible. You should too, since grants don’t need to be paid back, unlike loans. Grants helped save me a lot of money in the long run, especially when you factor in the cost of interest and fees on a loan.

TuitionHero Tip

And did you know about Federal Work-Study? This bonus program funds part-time roles for cash-strapped students to cover academic expenses.

What loans can graduate students take?

Graduate students are eligible for Direct Unsubsidized Loans and Direct PLUS Loans only, meaning interest starts accruing as soon as the loan is disbursed. Let's dive deeper.

Direct Unsubsidized Loans:

- You qualify regardless of your financial need.

- Interest accumulates while you're in school or during grace and deferment periods.

- Payments begin after graduation

- Graduate students can borrow up to $20,500 annually.

Direct PLUS Loans:

- These loans help cover costs not met by other financial aid.

- Schools determine award amounts based on attendance costs minus other financial aid received.

- They require a credit check.

- The interest rate for 2023-24 is 8.05%, higher than for the Direct Unsubsidized Loans

You can borrow more as a grad student than as an undergrad, but responsibility is key. Make sure you have a game plan for paying back those loans!

State and institutional aid programs

While federal aid via FAFSA is a cornerstone of grad-school funding, state and school programs can add thousands more to your package:

- State grant agencies: Many states run need-based grant programs for graduate students (e.g., California Cal Grants, New York’s TAP). Awards typically range from $1,000to $5,000 per year. Check your state’s higher-ed website for eligibility and deadlines when exploring whether FAFSA covers graduate school options.

- Institutional graduate fellowships: Departments often award competitive fellowships that include full-tuition waivers plus a living stipend (usually $10,000–$30,000 annually).

- Departmental scholarships: Beyond general fellowships, look for discipline-specific scholarships within your field (STEM, fine arts, social sciences). These smaller awards often have fewer applicants and can cover books, conference travel, or research expenses.

Employer tuition assistance & tax benefits

If you’re working while earning your master’s, your employer—and the IRS—can help shoulder the cost:

- Employer Tuition Reimbursement: Under IRS §127, up to $5,250 per year of employer-paid tuition assistance is tax-free. Some companies cover 100% of tuition in exchange for a service commitment—review your HR policy to see what’s on offer when pairing FAFSA for masters aid with workplace benefits.

- Lifetime Learning Credit (LLC): You can claim up to $2,000 per year in federal tax credits on qualified tuition and fees. Note: the credit phases out at higher income levels, so run the numbers or consult a tax advisor before filing—especially if you’ve used FAFSA masters degree loans and need extra relief.

- Tuition and Fees Deduction: If you don’t qualify for the LLC, you may still deduct up to $4,000 in tuition and fees directly from your taxable income, cutting your tax bill even if you can’t claim the credit.

Tax credits and deductions for graduate students

Graduate studies come with unique tax perks—make sure you claim everything you’re owed:

- Lifetime Learning Credit vs. AOTC: Grad students are only eligible for the Lifetime Learning Credit; the American Opportunity Tax Credit is reserved for undergraduates, so verify your eligibility when managing whether the FAFSA covers master's expenses.

- Student loan interest deduction: You can deduct up to $2,500 of interest paid on your grad-school loans each year, subject to income limits. Even small interest payments add up over time.

- 529 Plan distributions: Distributions from a 529 college-savings plan used for graduate tuition remain tax-free. If you (or loved ones) have been saving in a 529, now’s the time to tap it.

- Work-related education expenses: If your employer requires your degree to maintain or improve skills in your current job, you may deduct other education-related costs (transportation, books, supplies) as unreimbursed employee expenses—check Publication 970 for details.

Can graduate students avoid capitalized interest?

Another factor to consider is interest capitalization. That's what happens when any unpaid interest is added to your loan principal once your nonpayment period wraps up.

It's a good idea to pay down the interest while you're still in school. This strategy can help prevent a nasty surprise at the end of your grace period.

Compare private student loans now

TuitionHero simplifies your student loan decision, with multiple top loans side-by-side.

Compare Rates

Dos and don’ts of applying for FAFSA as a graduate student

Before diving into the nitty-gritty of the FAFSA application for graduate studies, let's consider some do's and don'ts. These quick tips will help make sure you maximize your opportunities for financial aid and avoid common pitfalls.

Do

Do apply early

Do report accurate financial information

Do actively seek out the available grants

Do have a plan for loan repayment

Do pay down interest while studying

Don't

Don't wait till the last minute

Don't overestimate your income

Don't limit yourself to loans

Don't borrow more than you can repay

Don't let interest capitalize unnecessarily

Advantages and disadvantages of applying for FAFSA as a graduate student

Applying for the FAFSA as a grad student can open doors to many financial aid opportunities. But, like most things, there are pros and cons tied to this process that you should consider.

- Increased loan limit: Graduate students can borrow a lot more funds than undergraduates.

- Grant opportunities: Graduates can apply for many federal grants, including the Fulbright and TEACH grants.

- Independence: Graduate students are considered independent and not reliant on their parents' financials.

- Higher interest rates: Grad students have to stomach higher interest rates on their loans compared to undergrads.

- No subsidized loan eligibility: Grad students are only eligible for unsubsidized loans and Direct PLUS Loans, meaning interest will begin accruing during school

- Pell Grant ineligibility: With the exception of those obtaining a post-baccalaureate teacher certification, grad students can't benefit from Pell Grants.

2025–26 FAFSA processing enhancements

In February 2025, the Department of Education rolled out batch‐correction capability for both the 2024–25 and 2025–26 FAFSA cycles—allowing schools to submit large files of ISIR updates via the Student Aid Internet Gateway.

By early March, it had processed over 1.5 million new 2025–26 submissions and delivered more than 7 million aid records to colleges and state agencies, significantly speeding error resolution and improving accuracy in financial aid packaging.

Why trust TuitionHero

At TuitionHero, we simplify college finances with Private Student Loans, Student Loan Refinancing, and FAFSA assistance, helping you reach your academic goals. Grad school can be expensive, but we can help you refinance your student loans to lower your interest rates. This makes it easier to pay off your debt. Start planning your financial future with TuitionHero today!

Frequently asked questions (FAQ)

The federal deadline for submitting your FAFSA form is June 30 of the school year you need help paying for. However, states and colleges may have their own deadlines, which can be much earlier. To make sure you get the most amount of aid possible, you should submit your FAFSA form as soon as possible after it becomes available on October 1 (this year it will be available in December).

Absolutely! In fact, graduate students with financial needs can benefit from the Federal Work-Study Program. This program offers part-time jobs, allowing students to earn money to help with school expenses.

As an independent student, you’ll apply for the FAFSA in the same way a graduate student does—by using only your financial information. At TuitionHero, we offer FAFSA Assistance to guide you through the whole process.

Yes, graduate students have many scholarship opportunities available to them. These can be based on field of study, demographic factors, academic accomplishments, and more. At TuitionHero, we can help you figure out where to find these scholarships and how to apply for them.

Yes, student loan refinancing is an option for both graduate and undergraduate students. It’s a smart move to lower interest rates and make paying back loans easier. TuitionHero has your back with our Student Loan Refinancing services to help you through it.

- Direct Unsubsidized Loans: Up to $20,500 per year for graduate students.

- Grad PLUS Loans: Up to your school’s total cost of attendance (no fixed cap).

- Aggregate limit: $138,500 total in unsubsidized federal loans across undergrad + grad.

- Research & test prep: Choose programs, note prerequisites and exam deadlines (GRE, GMAT, etc.).

- Finance plan: File FAFSA on Oct 1; explore state grants, institutional fellowships, and employer tuition aid.

- Applications: Secure recommendations, polish your personal statement, and submit all materials before deadlines.

- Skill building: Gain relevant experience, sharpen writing/research skills, and network with faculty.

Final thoughts

Pursuing a graduate degree is an investment in your future, and every dollar you secure outside of loans is that much less you’ll repay (with interest) down the road.

By combining federal FAFSA for grad school aid with state grants, institutional fellowships, employer assistance, and targeted tax breaks, you can craft a funding strategy that minimizes debt and maximizes opportunity.

Start early, stay organized, and tap into all available programs—your wallet (and peace of mind) will thank you.

Source

Author

Brian Flaherty

Brian is a graduate of the University of Virginia where he earned a B.A. in Economics. After graduation, Brian spent four years working at a wealth management firm advising high-net-worth investors and institutions. During his time there, he passed the rigorous Series 65 exam and rose to a high-level strategy position.

Editor

Rachel Lauren

Rachel Lauren is the co-founder and COO of Debbie, a tech startup that offers an app to help people pay off their credit card debt for good through rewards and behavioral psychology. She was previously a venture capital investor at BDMI, as well as an equity research analyst at Credit Suisse.

At TuitionHero, we're not just passionate about our work - we take immense pride in it. Our dedicated team of writers diligently follows strict editorial standards, ensuring that every piece of content we publish is accurate, current, and highly valuable. We don't just strive for quality; we aim for excellence.

Related posts

While you're at it, here are some other college finance-related blog posts you might be interested in.

5 minutes read

Can You Use FAFSA for Summer Classes or Graduate School?

Curious about using FAFSA beyond fall and spring semesters? Discover how to leverage federal aid for summer classes and graduate school, maximizing your educational funding opportunities.

Learn More

7 minutes read

How Does FAFSA Verify Assets and Does It Affect Eligibility for Aid?

How does FAFSA verify assets, and what documents are required? Learn the step-by-step FAFSA verification process, common mistakes to avoid, and expert tips to prepare.

Learn More

3 minutes read

Is FAFSA a Loan or a Grant? (Answered)

Learn about FAFSA and its role in accessing financial aid, and how it can help you secure grants, loans, and work-study opportunities for college.

Learn More

Shop and compare student financing options - 100% free!

Always free, always fast

TuitionHero is 100% free to use. Here, you can instantly view and compare multiple top lenders side-by-side.

Won’t affect credit score

Don’t worry – checking your rates with TuitionHero never impacts your credit score!

Safe and secure

We take your information's security seriously. We apply industry best practices to ensure your data is safe.

Finished scrolling? Start saving & find your private student loan rate today

Compare Personalized Rates