![]()

Advertiser Disclosure

Last update: June 6, 2025

8 minutes read

How Long Do Credit Inquiries Affect Your Credit Score?

Curious how long soft inquiries linger on your credit report and what that means for your score? Learn about the 1-year vs. 2-year windows for promotional and account-review pulls and get tips to manage your credit health.

By Brian Flaherty, B.A. Economics

Edited by Rachel Lauren, B.A. in Business and Political Economy

Learn more about our editorial standards

By Brian Flaherty, B.A. Economics

Edited by Rachel Lauren, B.A. in Business and Political Economy

Learn more about our editorial standards

When you check your credit or companies do it on your behalf, those pulls can show up on your report for months or even years. Understanding how much does a credit check affect your score can help you manage your financial health.

Knowing how long does a hard inquiry affect your credit score is just as important to avoid unwelcome surprises and plan your applications wisely.

Key takeaways

- Hard inquiries stay on your credit report for up to two years but only affect your score for a year

- Soft inquiries don’t affect your credit score and aren’t visible to lenders

- Shopping for certain loans within a short 14 to 45-day window minimizes the effect of multiple hard inquiries

How long do credit inquiries affect your credit score?

Credit inquiries, especially hard inquiries, can seem challenging. When a lender pulls your credit report to assess lending risk, a hard inquiry is made.

But how long do these inquiries affect your score? Generally, hard inquiries stay on your credit report for up to two years, but their effect on your score fades much faster.

Immediate effect of hard inquiries

A hard inquiry can reduce your credit score by up to five points, though this effect diminishes within a few months. The exact effect depends on your overall credit profile. For example, if you already have good to excellent credit, the drop is usually less significant.

Long-term effects

After about a year, the effect of that hard inquiry on your credit score is minimal. Most scoring models, including FICO, no longer consider it after 12 months. VantageScore, however, considers hard inquiries for two years. The inquiry itself also remains on your report for the full two years.

Multiple hard inquiries for the same type of loan

When shopping for the best mortgage or auto loan rates, multiple inquiries within a short time frame (usually 14 to 45 days) are typically treated as a single inquiry. This practice allows you to compare loans without being excessively penalized.

Other important questions

How to distinguish between hard and soft inquiries?

Understanding the difference between hard and soft inquiries is vital. A soft inquiry, like when you check your own credit report or when employers pull your report for background checks, doesn’t affect your credit score.

TuitionHero Tip

Soft inquiries aren’t visible to potential lenders and have no effect on your creditworthiness. For more details, check out our resources on student loans.

Promotional vs. account-review soft inquiries

Not all soft pulls are the same—understanding the two main types can help you interpret your credit report and know how long do hard inquiries affect credit score or clear them out.

1. Promotional inquiries

- Triggered when lenders, card issuers, or insurers pre-approve you for an offer (e.g., “pre-qualified” credit cards, loan offers, insurance discounts).

- Only limited information is exchanged—often just your name, address and summary score data.

- Lifespan: Typically fall off your report after one year, so you’ll see how long credit inquiries affect credit score clearly.

- Score impact: Always zero—these never affect your credit score.

2. Account-review inquiries

- Occur when an existing creditor or service provider checks your full credit file for marketing (e.g., credit-line increase), underwriting (e.g., utility deposit decision) or account-management purposes.

- Pull full credit details, similar to a hard inquiry, but still zero impact—though they can make you wonder how many points does credit inquiries lower your score if you don’t realize they’re soft.

- Lifespan: Remain on your report for two years, matching hard pulls and answering the question, "How long do hard inquiries last?"

- Score impact: Zero, but they “clutter” your inquiry history.

TuitionHero Tip

If you see a cluster of pre-approval pulls, know they usually vanish in 12 months—and never ding your score. Account-review pulls stick around twice as long, so if you’re concerned about the appearance of too many inquiries, ask each provider whether they’re doing a promotional or account-review check before you proceed.

How can I reduce the effect of hard inquiries?

Reducing the effect of hard inquiries involves strategic planning:

- Limit applications: Only apply for credit when necessary.

- Shop within a narrow window: If you’re rate shopping for auto loans or mortgages, do so within a condensed period to minimize multiple inquiries.

- Monitor your credit: Regularly check your credit report for any unauthorized hard inquiries.

Can I dispute a hard inquiry?

You can't remove a legitimate hard inquiry from your report. But if you come across one you don't recognize, it could be a sign of identity theft.

In such cases, you can dispute the inquiry. For more on handling disputes and removing inaccuracies, consider services offering FAFSA assistance.

Understanding the difference between hard and soft inquiries

Hard and soft inquiries differ significantly in their effect on your credit report. Hard inquiries occur when lenders check your credit for applications like mortgages, credit cards, or other types of loans.

They can lower your credit score by up to five points and stay on your report for up to two years. However, they usually lose their effect after the first 12 months.

In contrast, soft inquiries happen when you check your credit score yourself or when businesses review your credit for pre-approved offers. These don't affect your credit score.

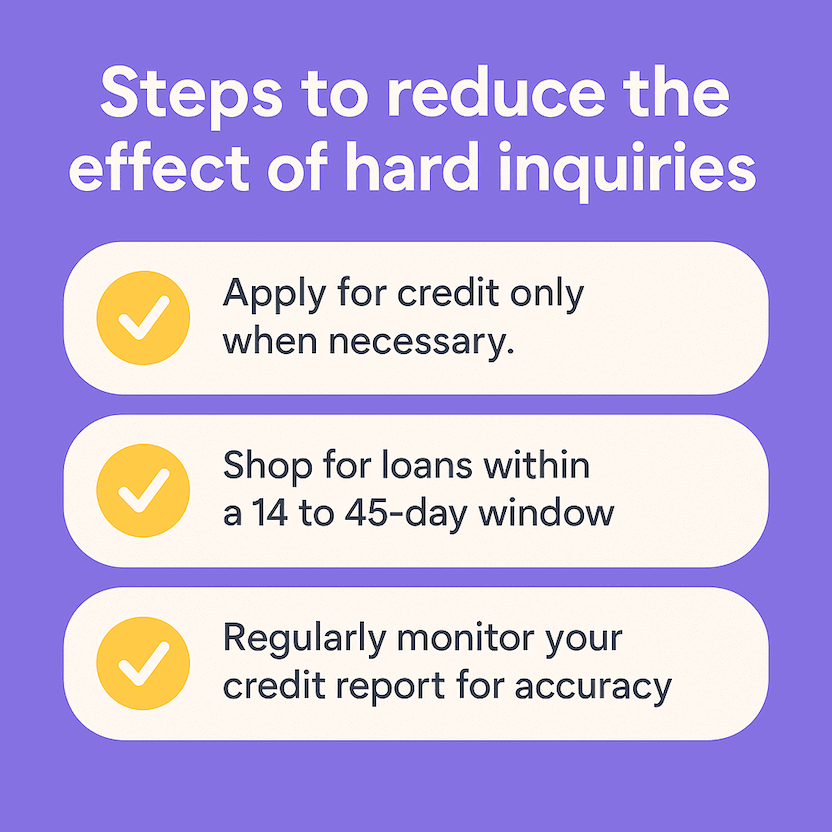

Steps to reduce the effect of hard inquiries

There are several methods to minimize the effect of hard inquiries before applying for significant loans:

- Apply for credit only when necessary.

- If you’re shopping for a loan, do so within a short window to limit multiple inquiries' effect.

- Regularly monitor your credit report for accuracy.

TuitionHero Tip

Using these steps can protect your credit score from dropping unnecessarily. For more strategies, consider learning about the best credit card for your needs.

How hard inquiries affect loan shopping

When applying for major loans like a mortgage or auto loan, you might worry about multiple hard inquiries. However, credit scoring models like FICO and VantageScore group multiple inquiries as one if they occur within a 14 to 45-day window. This grouping permits you to shop around for the best rates without damaging your credit score.

Effect of multiple hard inquiries

Applying for several types of credit within a short period can cause more issues. If a lender sees numerous hard inquiries for different types of credit like credit cards, personal loans, or home equity loans, they might suspect financial trouble.

Having too many hard inquiries may signal financial instability to lenders. This perceived risk can result in higher interest rates or even loan denials.

Compare private student loans now

TuitionHero simplifies your student loan decision, with multiple top loans side-by-side.

Compare Rates

Disputing inaccurate inquiries

It's possible to encounter hard inquiries you don’t recognize, which may indicate identity theft. Disputing such inquiries involves contacting the credit bureau to have them removed. Legitimate inquiries remain for the two-year period, but inaccurate ones can be disputed.

Below is a table summarizing important data about credit inquiries' effects and timelines to provide a clear understanding:

Type of Inquiry | Credit Score Impact | Duration on Report | Typical Applications |

|---|---|---|---|

Hard Inquiry | Up to 5 points | Up to 2 years | Mortgages, credit cards, loans |

Soft Inquiry | None | Not recorded | Checking own score, pre-approvals |

Grouped Inquiries | Minimal (if within 14-45 days) | Up to 2 years | Mortgage or auto loan shopping |

Understanding these dynamics enhances your ability to navigate financial decisions and manage your credit score effectively.

Dos and don’ts of managing credit inquiries

When managing credit inquiries, it’s essential to navigate the process smartly to protect your credit score. Below are critical dos and don'ts to help you avoid pitfalls and make informed decisions.

Do

Check your credit report regularly

Shop for loans within a 14 to 45-day window

Dispute unauthorized hard inquiries

Keep credit card balances low

Use credit monitoring services

Don't

Apply for multiple types of credit in a short timeframe

Ignore inaccuracies on your credit report

Panic over a single hard inquiry

Close old credit accounts suddenly

Apply for new credit if planning a big loan soon

Advantages and disadvantages of monitoring your credit score

Monitoring your credit score has different benefits and drawbacks. Understanding these can help you decide how best to manage and improve your credit effectively.

- Early fraud detection: Identifies unauthorized activity quickly.

- Better loan terms: Maintains a higher score for favorable interest rates.

- Educational: Understand the credit scoring process better.

- Potential obsession: Constant checking can lead to undue stress.

- False sense of security: Regular monitoring doesn’t prevent fraud.

- Cost: Some monitoring services charge fees.

CFPB’s medical-debt removal postponed

On February 6, 2025, the Eastern District of Texas granted a 90-day stay, delaying the CFPB’s rule banning medical debt from credit reports from March 17 to June 15, 2025. The rule—finalized January 7, 2025—had aimed to remove roughly $49 billion in medical debts affecting 15 million consumers.

Litigation by ACA International and Specialized Collection Systems under the APA prompted the stay. As of May 2025, the CFPB has moved to cancel the rule entirely, so the June 15 effective date remains uncertain .

Until then, any hard or soft inquiries tied to medical-debt disputes will continue to appear on consumer files. Once in effect, all medical-debt inquiries will be removed, potentially boosting affected consumers’ scores.

Why trust TuitionHero

At TuitionHero, we help students and parents navigate financial landscapes and manage student loans. Our platform connects you to lenders for private loans, refinancing, and scholarships. We simplify the FAFSA process and offer student-friendly credit cards. Use our services to improve your financial health and ensure a smooth educational journey.

Frequently asked questions (FAQ)

Too many hard inquiries within a short period could signal financial instability to lenders, potentially resulting in higher interest rates or denial of credit applications. It's crucial to manage your credit applications wisely to avoid raising red flags.

While legitimate hard inquiries can’t be removed from your credit report, you can dispute any inaccuracies. If a hard inquiry appears that you don’t recognize, contact the credit bureau to investigate and potentially remove it.

When shopping for loans, credit scoring models like FICO group multiple inquiries within a short timeframe (14 to 45 days) into a single inquiry. This practice allows you to compare loan offers without significantly hurting your credit score.

No. Soft inquiries are legitimate, informational checks (like when you pull your own report or get pre-qualified offers) and have no impact on your score. They’re managed by the credit bureaus and automatically drop off over time—you can’t manually delete them.

Generally, no. Most lenders can’t see soft inquiries except their own.

They only view hard inquiries (which occur when you apply for credit). Soft pulls are invisible to outside creditors and don’t factor into loan or card approvals.

Final thoughts

Credit inquiries are a normal part of financial life, but they don’t have to be mysterious or harmful. Even though individual hard pulls can lower your score by up to 5–10 points—answering how much does a hard inquiry affect your credit score—they lose weight after a year, and vanish completely in two years.

By distinguishing between hard pulls and the two types of soft pulls—promotional and account review—you can shop for loans strategically, dispute any unauthorized inquiries, and focus on the factors that truly build a strong credit profile.

Source

Author

Brian Flaherty

Brian is a graduate of the University of Virginia where he earned a B.A. in Economics. After graduation, Brian spent four years working at a wealth management firm advising high-net-worth investors and institutions. During his time there, he passed the rigorous Series 65 exam and rose to a high-level strategy position.

Editor

Rachel Lauren

Rachel Lauren is the co-founder and COO of Debbie, a tech startup that offers an app to help people pay off their credit card debt for good through rewards and behavioral psychology. She was previously a venture capital investor at BDMI, as well as an equity research analyst at Credit Suisse.

At TuitionHero, we're not just passionate about our work - we take immense pride in it. Our dedicated team of writers diligently follows strict editorial standards, ensuring that every piece of content we publish is accurate, current, and highly valuable. We don't just strive for quality; we aim for excellence.

Related posts

While you're at it, here are some other college finance-related blog posts you might be interested in.

4 minutes read

How to Build Credit as a Student in 2025

Wondering how to build credit as a student in 2025? Discover expert tricks to kickstart your score with cards, loans, and smart habits. Set yourself up for success now!

Learn More

6 minutes read

How to Get Your First Credit Card

Are you ready to navigate the journey of getting your first credit card? Learn the essentials step by step to avoid common pitfalls.

Learn More

6 minutes read

What is a Balance Transfer? How to Lower Credit Card Debt in 2024

Learn about balance transfers to slash debt and boost savings. Discover how to consolidate debt, save money on interest, and take control of your finances today!

Learn More

Shop and compare student financing options - 100% free!

Always free, always fast

TuitionHero is 100% free to use. Here, you can instantly view and compare multiple top lenders side-by-side.

Won’t affect credit score

Don’t worry – checking your rates with TuitionHero never impacts your credit score!

Safe and secure

We take your information's security seriously. We apply industry best practices to ensure your data is safe.

Finished scrolling? Start saving & find your private student loan rate today

Compare Personalized Rates