![]()

Advertiser Disclosure

Last update: September 24, 2025

10 minutes read

What's the Deal with Income Share Agreements? Are They Actually Better Than Student Loans?

Wondering if Income Share Agreements are better than student loans? Learn how ISAs work, their pros and cons, and what new 2024 rules mean for you.

By Derick Rodriguez, Associate Editor

Edited by Yerain Abreu, M.S.

Learn more about our editorial standards

By Derick Rodriguez, Associate Editor

Edited by Yerain Abreu, M.S.

Learn more about our editorial standards

So you're trying to figure out if Income Share Agreements could replace your student loans? Yeah, I get it – the whole student debt thing is pretty overwhelming. Let me break down how ISAs actually work and whether they're worth your time.

Here's the basic idea: instead of borrowing money that you'll definitely have to pay back (even if you end up working at a coffee shop for two years), you agree to pay back a percentage of whatever you actually earn. Sounds pretty reasonable, right?

This whole financing thing has been getting more attention lately as students look for literally anything better than traditional loans. But here's where I need to be real with you: ISAs have their own weird benefits and some pretty serious risks that you absolutely need to understand before you sign anything.

Oh, and plot twist: as of 2024, the government now treats ISAs like private education loans, which actually gives you way more protection than before.

Key takeaways

- ISAs take a percent of income, not fixed payments, with no interest

- They can cost more if you earn high and are only offered in limited programs

- Federal loans usually offer better protections, so compare both before choosing

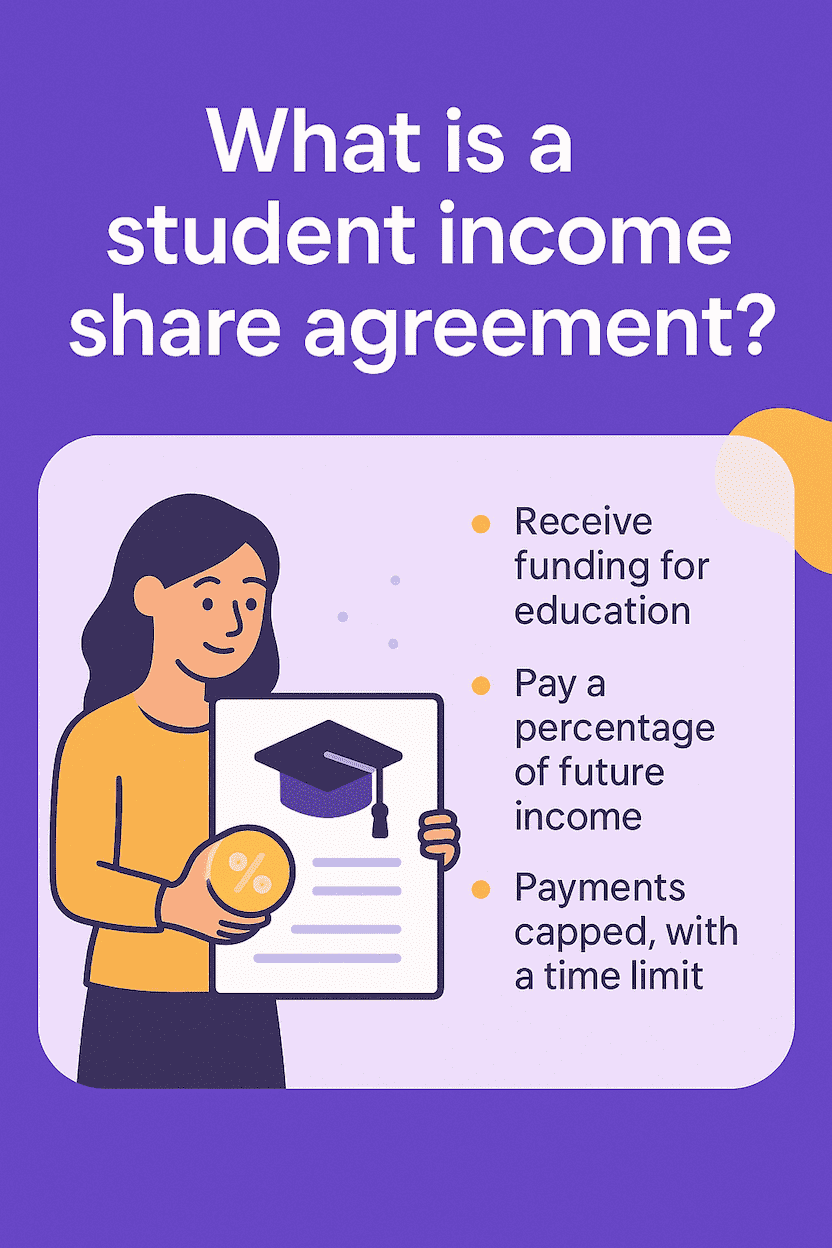

What is a student income share agreement?

Think of it like this: someone basically invests in your education upfront, and you pay them back later based on how much money you're actually making after you graduate.

The simple version goes like this: Instead of borrowing $30,000 that you have to pay back no matter what happens to your life, an ISA means you only pay when you're actually earning decent money.

Land a great job? You'll pay more. Can't find work or stuck making $25K? You pay way less or maybe nothing at all.

It's kinda like having a business partner for your education. They're betting on you because they think you'll do well, and honestly, they only make money if you do too.

Here's how the whole thing works:

- Someone covers your school costs upfront (nice, right?)

- After graduation, you give them a slice of every paycheck for a few years

- Payments stop after a set time period or when you've paid back enough

- Not making much? Then you don't pay anything that month

You might hear people call these "income sharing" or "pay-it-forward" programs, but they're basically the same thing with different names.

How do these things actually work?

ISAs work pretty differently from regular student loans. With a normal loan, you borrow money and pay it back with interest; it doesn't matter if you're unemployed or making bank. With an ISA, your payments actually change based on what you're bringing home.

Here's the timeline:

- Before school starts: You sign something saying you'll pay a certain percentage of your future salary. Could be 5%, could be 10% – depends on the program.

- While you're in school: The ISA people pay your school. You're not paying anything yet, which is honestly pretty sweet.

- After you graduate: You start making monthly payments based on your actual paycheck. Making $3,000 a month and owe 5%? That's $150 that month.

Most ISAs come with these features:

- Minimum income threshold: Don't make enough (usually around $20,000/year)? You don't owe anything

- Time limit: Payments stop after a certain number of years, even if you haven't paid back the "full" amount

- Payment cap: There's usually a maximum you'll ever pay, even if you become the next tech billionaire

TuitionHero Tip

If you lose your job or your income drops, your ISA payments automatically go down or stop until your income recovers.

ISAs vs. regular student loans: What's the difference?

The big difference is pretty straightforward: student loans make you pay the same amount every single month, regardless of your situation. ISAs actually adjust based on what you're earning.

Regular student loans:

- Same payment every month for years and years

- Interest keeps getting added, making your total debt bigger

- Unemployed? Too bad, you still owe money

- You know exactly what you'll pay each month (which some people actually prefer)

- Federal loans have income-driven plans and forgiveness options

Income Share Agreements:

- Payments go up and down with your paycheck

- No interest getting added to your debt

- Low-income months? You might pay zero

- Your payment changes month to month

- Now they're regulated as private education loans (which is actually good for you)

Here's an example that might make this clearer: Say you owe $500/month on a regular loan. Whether you make $2,000 or $5,000 that month, you're paying $500.

With an ISA at 10%, you'd pay $200 if you earned $2,000 or $500 if you earned $5,000.

The risk profile is totally different. Loans give you predictability but zero flexibility. ISAs give you flexibility but less predictability about your total costs.

Compare private student loans now

TuitionHero simplifies your student loan decision, with multiple top loans side-by-side.

Compare Rates

Who's actually offering ISAs these days?

Okay, here's where things get interesting (and a bit messy). You can't just walk into any school and get an ISA like you can with federal loans. The market's gotten pretty turbulent lately.

- Coding bootcamps and training programs: A bunch of coding schools offer ISAs, though way fewer than a couple of years ago. Quick warning: some big names like Bloom Institute of Technology (used to be Lambda School) got slammed by federal regulators in 2024 for basically lying to students and got shut down from doing ISAs.

- Some regular colleges: A few universities, like Purdue, have ISA options alongside normal financial aid, but it's still pretty rare.

- Specialized training companies: Companies teaching stuff like web design, digital marketing, or cybersecurity sometimes use ISAs.

- Third-party ISA companies: Some companies will partner with schools to provide ISA funding even if the school doesn't offer it directly.

Most ISA programs focus on job training that leads to decent-paying work relatively quickly. You'll see them more for tech jobs, healthcare training, and skilled trades than for your typical four-year degree.

Always research current providers really carefully. The regulatory crackdown has been pretty intense, and you don't want to get stuck with a sketchy company.

TuitionHero Tip

You might hear ISAs called different names like "income sharing" or "pay-it-forward" programs, but they all work the same way.

Are ISAs actually worth it?

This really depends on your specific situation and career plans. They work great for some people and are terrible for others.

ISAs might make sense if:

- You're studying something that typically leads to good jobs (coding, healthcare, etc.)

- You're stressed about taking on debt you might not be able to handle

- You like the idea that payments match what you actually earn

- The school has a solid track record of job placement

- You can't get federal student loans for whatever reason

Stick with regular loans if:

- You can get federal student loans (usually 3-5% interest with way better protections)

- You're unsure about your career path or earning potential

- The ISA terms look like you'd pay significantly more than a loan

- You prefer knowing exactly what you'll pay each month

- You want the option to pay off debt early and save money

The key question: Do you think you'll make good money after graduation?

If yes, an ISA will probably cost you more long-term. If you're not confident or worried about job prospects, an ISA gives you protection that loans don't.

Always run the numbers for different scenarios. What would you pay with an ISA versus loans if you made $30K, $50K, or $80K per year?

Red flags and things to watch out for

ISAs aren't perfect, and there's some stuff that could really mess with you later.

- Provider legitimacy: With all the recent regulatory drama, you need to research any company thoroughly before signing anything. Some have been shut down for straight-up lying to students.

- Income reporting hassle: Every year, you'll need to prove how much you make. If you're freelancing or have multiple income sources, this can be a real pain.

- Career restrictions: Some ISAs have rules about what jobs you can take. They might not let you switch to a lower-paying field, even if that's what would make you happy.

- Tax weirdness: Even though ISAs are regulated as loans now, tax treatment can still be confusing. You might want to talk to someone who knows tax stuff.

- International enforcement: Move to another country? The ISA company can still come after you, though it's harder for them to actually collect.

- High earner penalty: If your career really takes off, you might end up paying way more than you would've with a traditional loan.

The regulatory situation (this is actually important)

Here's something the original version of this info didn't mention: the Consumer Financial Protection Bureau now treats ISAs as private education loans under federal law. This happened because some providers were being pretty shady.

What this means for you:

- ISA companies have to follow stricter rules about what they tell you

- You have more legal protections than before

- Misleading marketing can get companies in serious federal trouble

- Some providers have already been fined or shut down

Who knew federal regulation could actually be helpful?

The pros and cons of income share agreements

ISA Pros | ISA Cons |

|---|---|

Payments match your actual income | Limited availability |

No interest charges | Might cost more if you do well |

Protection if you're unemployed | Complex income reporting |

Predictable percentage rate | Career flexibility restrictions |

Debt doesn't grow over time | Provider/market instability |

Better regulation now | Potentially higher total cost |

Why trust TuitionHero

At TuitionHero, we help you find the best private student loans by comparing top lenders and breaking down eligibility, interest rates, and repayment options. Whether you need additional funding beyond federal aid or a loan without a cosigner, we simplify the process. We also provide expert insights on refinancing, FAFSA assistance, scholarships, and student credit cards to support your financial success.

Frequently asked questions (FAQ)

Usually yes, but the rules vary a lot. Some make you pay the full amount you would've paid anyway, which kinda defeats the purpose of paying early. Others actually let you save money by paying it off faster.

If you're not making enough (usually under $20K/year), you don't pay anything. Though you might have to extend your payment period later to make up for the missed months.

Tax treatment is still pretty murky. Even though they're regulated as loans now, the specific deductions might not apply. Probably worth asking someone who knows tax law.

Nope. They're mostly for bootcamps, job training, and some specific college programs. You probably can't get one for a regular four-year degree.

You still owe the money, and they'll still try to collect it. Moving doesn't magically make your ISA disappear.

Do your homework. Check for regulatory actions, read all the fine print, and maybe talk to a financial aid counselor before signing anything.

Final thoughts

Income Share Agreements can be smart if you want protection from payments you can't afford and don't want to deal with interest. But they're definitely not always better than regular student loans, and the whole market has been pretty chaotic with all the regulatory enforcement lately.

What makes sense depends on your career plans and how confident you are about future earnings. If you're studying something that usually leads to high-paying jobs, you'll probably end up paying more with an ISA.

Here's my advice: exhaust your federal student loan options first. Those typically have better terms and way more protections.

If you're still considering an ISA after that, research providers like your financial future depends on it (because it does), and remember that you're now protected by federal lending rules.

Don't just pick the first option that sounds good. Compare ISAs, federal loans, and whatever other financing you can find. Your future self will thank you for doing the math now instead of just hoping for the best.

Source

Author

Derick Rodriguez

Derick Rodriguez is a seasoned editor and digital marketing strategist specializing in demystifying college finance. With over half a decade of experience in the digital realm, Derick has honed a unique skill set that bridges the gap between complex financial concepts and accessible, user-friendly communication. His approach is deeply rooted in leveraging personal experiences and insights to illuminate the nuances of college finance, making it more approachable for students and families.

Editor

Yerain Abreu

Yerain Abreu is a Content Strategist with over 7 years of experience. He earned a Master's degree in digital marketing from Zicklin School of Business. He focuses on college finance, a niche carved out of his journey through the complexities of academic finance. These firsthand experiences provide him with a unique perspective, enabling him to create content that's informative and relatable to students and their families grappling with the intricacies of college financing.

At TuitionHero, we're not just passionate about our work - we take immense pride in it. Our dedicated team of writers diligently follows strict editorial standards, ensuring that every piece of content we publish is accurate, current, and highly valuable. We don't just strive for quality; we aim for excellence.

Related posts

While you're at it, here are some other college finance-related blog posts you might be interested in.

3 minutes read

Where Did Morgan Wallen Go to College? The Unexpected Path of a Country Star

Did Morgan Wallen go to college? See how a baseball injury changed his plans and how students can learn from his journey.

Learn More

5 minutes read

How to Build a Strong Resume for Internships

Wondering how to craft a compelling internship resume that grabs attention? Discover essential strategies to build a standout resume and secure your dream internship.

Learn More

8 minutes read

How to Get Your Student Loans Forgiven

Learn how to erase student loan debt with our top strategies for Public Service Loan Forgiveness, including employer tips and payment plans.

Learn More

Shop and compare student financing options - 100% free!

Always free, always fast

TuitionHero is 100% free to use. Here, you can instantly view and compare multiple top lenders side-by-side.

Won’t affect credit score

Don’t worry – checking your rates with TuitionHero never impacts your credit score!

Safe and secure

We take your information's security seriously. We apply industry best practices to ensure your data is safe.

Finished scrolling? Start saving & find your private student loan rate today

Compare Personalized Rates