![]()

Advertiser Disclosure

Last update: September 24, 2025

4 minutes read

What Is FIRE for Students? The Early Retirement Movement Starting in College

Could you retire by 35 while your classmates are still paying off student loans? Learn how the FIRE movement is reshaping financial planning for college students.

By Derick Rodriguez, Associate Editor

Edited by Yerain Abreu, M.S.

Learn more about our editorial standards

By Derick Rodriguez, Associate Editor

Edited by Yerain Abreu, M.S.

Learn more about our editorial standards

Could you coast toward work-optional by 35 while your friends are still wrestling loan servicers? Maybe. Plot twist: the big lever isn’t a secret stock pick; it’s time plus boring consistency.

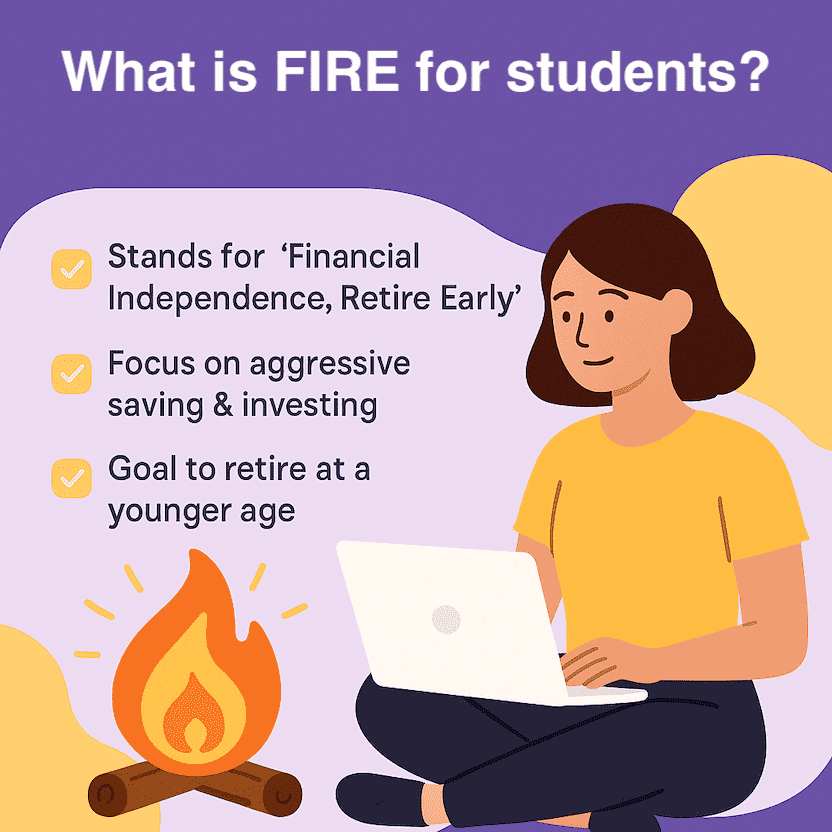

FIRE (Financial Independence, Retire Early) isn’t just for engineers with absurd RSUs anymore; students can stack a head start while they’re still living on instant noodles.

Key takeaways

- FIRE means saving about 25x your yearly spending to retire early

- Starting young lets even small investments grow a lot over time

- Pay off high-interest loans before investing heavily

What FIRE really is (and what folks get wrong)

FIRE uses a rule-of-thumb target of ~25x your annual spending, tied to a ~4% initial withdrawal in year one and then inflation adjustments, not because “stocks do 7% real,” but because of historical portfolio tests for ~30-year retirements begun by

Bengen and later popularized via the Trinity work. If your plan is 40–60 years (early retirement), many people nudge down to ~3–3.5% for safety. Same math, different risk vibe.

Want to figure out your FIRE number? Just multiply your yearly expenses by 25 (that's thanks to the 4% rule). So, if you spend $40,000 a year, you're aiming for a cool $1,000,000.

Keep in mind, though, this is just a starting point, and you'll want to think about sequence risk too.

TuitionHero Tip

The 4% rule was designed for 30-year retirements, so early retirees may want to use a more conservative 3-3.5% rate for longer retirement periods.

Why students actually have an edge (the compounding thing)

Starting in your early 20s often beats starting bigger in your 30s because compounding gets extra “laps.” If you want to see the gap with your own numbers, try the SEC compound interest calculator (plug “start at 20” vs “start at 30,” same rate). It’s a little dizzying when you see the curves diverge.

2025–26 reality check on student-loan rates

For new federal loans disbursed July 1, 2025–June 30, 2026: 6.39% undergrad Direct, 7.94% grad Direct, 8.94% PLUS. If your APR is ~7–9%, prepaying high-rate debt can be a risk-free “return” that often beats expected market returns—cold math, no hype.

Planning on government or qualifying nonprofit work? PSLF can zero your remaining federal balance after 120 qualifying payments.

Verify your employer and repayment plan via the PSLF Help Tool and program page here. Rules and policies are subject to change, so always verify the latest regulations before relying on forgiveness for your financial planning.

Compare private student loans now

TuitionHero simplifies your student loan decision, with multiple top loans side-by-side.

Compare Rates

How to start (without a salary yet)

- Automate something tiny. Even $25–$50/mo into a broad index fund builds the habit; commission-free platforms reduce friction.

- Use a Roth IRA if eligible. You need earned income to contribute; for 2025 the IRA limit is $7,000 (<50). (If you don’t have earned income: a Roth IRA contribution isn’t allowed unless a spousal IRA with joint filing, which, let’s be real, most students won’t have.)

- Anchor expectations in history, not wishful thinking. Long-run U.S. stocks show ~6–7% real, depending on the period.

TuitionHero Tip

Use your student status to get discounts on everything from software to car insurance. Every dollar saved is a dollar that can be invested.

Lean vs. Traditional vs. Fat FIRE

Lean = lower spend, Traditional = middle-ish, Fat = higher spend. These are community labels, not universal dollar lines, so translate them into your budget and run the same 25x math.

Mini-plan you can actually follow

- To figure out your initial FIRE number, track your spending for a month, then multiply that by twelve.

- Choose a starting SWR: 4% if you’re fine with the classic 30-year tests; ~3–3.5% if you want more cushion for a much longer horizon.

- Open accounts, automate a small transfer, and compare your loan APR to expected returns before deciding invest vs. prepay.

- Re-run your numbers each semester as income/aid/housing changes. (Yes, your budget will morph; it’s supposed to.)

Why trust TuitionHero

At TuitionHero, we help you find the best private student loans by comparing top lenders and breaking down eligibility, interest rates, and repayment options. Whether you need additional funding beyond federal aid or a loan without a cosigner, we simplify the process. We also provide expert insights on refinancing, FAFSA assistance, scholarships, and student credit cards to support your financial success.

Frequently asked questions (FAQ)

Depends on your interest rate and job track. At ~7–9%, prepaying loans is a strong “return.” If you’re PSLF-eligible, confirm employer + repayment plan in the Help Tool before leaning into minimums + investing.

If you can do $25–$50/mo automatically without wrecking rent/food, yes; habits trump waiting for the “perfect” moment. Commission-free helps for tiny buys.

Most students are in low brackets, so Roth can be sweet if you have earned income. No earned income = no Roth contribution. Limits and rules live at the IRS links above.

Use a conservative real return (e.g., ~5% nominal after fees/inflation), then sanity-check against long-run data like Damodaran’s series; don’t copy a bull-market decade and call it “normal.”

Final thoughts

FIRE in college isn’t about misery or being a spreadsheet robot. It’s about giving your future self that delicious option set: fewer money-driven decisions, more freedom to pick work that fits.

Start small, stay skeptical, let time do the heavy lifting. If your “retire by 35” slips to 42? That’s not failure, that’s life… still work-optional sooner than most.

Source

- FIRE movement - Wikipedia

- What is the Financial Independence, Retire Early (FIRE) Movement?

- FIRE | Financial independence Retire early | Fidelity

- (DL-25-03) Interest Rates for Direct Loans First Disbursed Between July 1, 2025 and June 30, 2026

- Public Service Loan Forgiveness (PSLF) Help Tool | Federal Student Aid

Author

Derick Rodriguez

Derick Rodriguez is a seasoned editor and digital marketing strategist specializing in demystifying college finance. With over half a decade of experience in the digital realm, Derick has honed a unique skill set that bridges the gap between complex financial concepts and accessible, user-friendly communication. His approach is deeply rooted in leveraging personal experiences and insights to illuminate the nuances of college finance, making it more approachable for students and families.

Editor

Yerain Abreu

Yerain Abreu is a Content Strategist with over 7 years of experience. He earned a Master's degree in digital marketing from Zicklin School of Business. He focuses on college finance, a niche carved out of his journey through the complexities of academic finance. These firsthand experiences provide him with a unique perspective, enabling him to create content that's informative and relatable to students and their families grappling with the intricacies of college financing.

At TuitionHero, we're not just passionate about our work - we take immense pride in it. Our dedicated team of writers diligently follows strict editorial standards, ensuring that every piece of content we publish is accurate, current, and highly valuable. We don't just strive for quality; we aim for excellence.

Related posts

While you're at it, here are some other college finance-related blog posts you might be interested in.

3 minutes read

Where Did Morgan Wallen Go to College? The Unexpected Path of a Country Star

Did Morgan Wallen go to college? See how a baseball injury changed his plans and how students can learn from his journey.

Learn More

5 minutes read

How to Build a Strong Resume for Internships

Wondering how to craft a compelling internship resume that grabs attention? Discover essential strategies to build a standout resume and secure your dream internship.

Learn More

8 minutes read

How to Get Your Student Loans Forgiven

Learn how to erase student loan debt with our top strategies for Public Service Loan Forgiveness, including employer tips and payment plans.

Learn More

Shop and compare student financing options - 100% free!

Always free, always fast

TuitionHero is 100% free to use. Here, you can instantly view and compare multiple top lenders side-by-side.

Won’t affect credit score

Don’t worry – checking your rates with TuitionHero never impacts your credit score!

Safe and secure

We take your information's security seriously. We apply industry best practices to ensure your data is safe.

Finished scrolling? Start saving & find your private student loan rate today

Compare Personalized Rates