![]()

Advertiser Disclosure

Last update: October 14, 2025

8 minutes read

What is Dollar-Cost Averaging Crypto? The Student Strategy for Bitcoin Investing

Are you a student curious about investing in cryptocurrency but worried about market volatility? Discover how dollar-cost averaging can make crypto investing more manageable and less stressful for your budget.

By Derick Rodriguez, Associate Editor

Edited by Brian Flaherty, B.A. Economics

Learn more about our editorial standards

By Derick Rodriguez, Associate Editor

Edited by Brian Flaherty, B.A. Economics

Learn more about our editorial standards

Ever watched Bitcoin's price swing from $30,000 to $70,000 and back down again, wondering if there's a way to invest without losing sleep over every market move? You're not alone. Cryptocurrency markets are notoriously volatile, which can make timing your investments feel like trying to catch a falling knife.

This post will break down dollar-cost averaging (DCA) for cryptocurrency investing, explain why it works particularly well for students on tight budgets, and show you how to set up your own DCA strategy without breaking the bank.

Key takeaways

- Dollar-cost averaging spreads crypto purchases over time, reducing the impact of price swings on your overall investment

- Students benefit from DCA because it requires smaller, regular investments rather than large lump sums

- DCA removes the stress of timing the market, making it ideal for beginners who want exposure to crypto

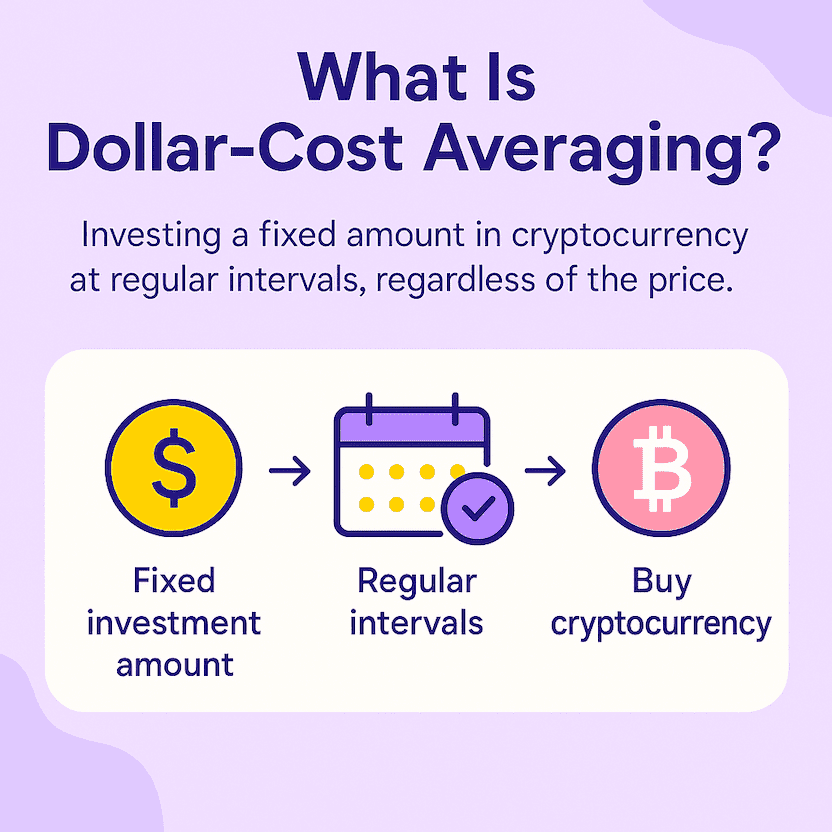

What is dollar-cost averaging in crypto investing?

Dollar-cost averaging means investing a fixed amount of money into cryptocurrency at regular intervals, regardless of the current price. Instead of trying to time when Bitcoin is "cheap," you buy the same dollar amount every week, month, or pay period.

This approach removes emotion and guesswork from your investing decisions. Rather than stressing about whether today is the perfect day to buy Bitcoin, you stick to a predetermined schedule that spreads your purchases across different market conditions.

How does dollar-cost averaging work for crypto investing?

Here's how it works:

Let's say you decide to invest $50 in Bitcoin every month.

- In January, Bitcoin costs $40,000, so you get 0.00125 BTC.

- In February, the price drops to $30,000, so your $50 buys 0.00167 BTC.

- In March, Bitcoin jumps to $50,000, and you get 0.001 BTC.

Over time, you're buying more Bitcoin when prices are low and less when they're high.

TuitionHero Tip

Many students worry they need thousands of dollars to start investing in crypto. With DCA, you can start with as little as $10-25 per week and still build meaningful positions over time.

The beauty of DCA lies in its simplicity. You don't need to analyze charts, predict market movements, or stress about whether today is the "right" day to buy. Your investment schedule does the work for you.

Why students should consider DCA for Bitcoin and crypto

Students face unique financial challenges that make DCA particularly attractive compared to other investment strategies.

- Limited capital: Most students don't have $5,000 sitting around to make a big crypto purchase. DCA lets you invest your spare money from part-time jobs, internships, or allowances without waiting to accumulate a large sum.

- Irregular income: Student income often comes in chunks (like financial aid disbursements) or varies month to month. DCA can adapt to your cash flow by adjusting investment amounts during busy or slow periods.

- Learning while doing: DCA gives you skin in the game without requiring deep market knowledge upfront. You'll naturally learn about crypto markets while your investment grows, making it an educational experience.

- Reduced emotional stress: Watching your $2,000 Bitcoin purchase lose 20% value overnight is gut-wrenching. Losing $50 on a monthly DCA purchase? Much more manageable psychologically.

TuitionHero Tip

Consider timing your DCA purchases with your payday or when financial aid hits your account. This creates a natural rhythm and ensures you're investing money you can actually afford to lose if Bitcoin crashes.

Compare private student loans now

TuitionHero simplifies your student loan decision, with multiple top loans side-by-side.

Compare Rates

How to start your crypto DCA plan

Creating an effective DCA plan requires answering a few key questions about your goals, budget, and risk tolerance.

- Choose your investment amount: Start with an amount you won't miss. For most students, this might be $25-100 per month. Remember, you can always increase this amount later as your income grows.

- Pick your frequency: Weekly purchases tend to smooth out volatility better than monthly ones, but they also mean more transaction fees. Monthly purchases work well for most students and align with typical income patterns.

- Select your cryptocurrency: Bitcoin remains the most popular DCA choice for cryptocurrency due to its market dominance and continued popularity compared to smaller tokens. Ethereum is another potential option. Avoid spreading your initial DCA across too many different coins.

- Set up automation: Most major crypto exchanges offer recurring purchase features. Automating your DCA removes the temptation to skip purchases during market downturns or double up during rallies.

TuitionHero Tip

Start your DCA during a neutral or down market if possible. Beginning during a major rally means your first few purchases happen at higher prices, though this evens out over time.

Top crypto exchanges for student DCA investing

Several platforms cater well to student investors looking to implement DCA strategies.

- Coinbase: Offers recurring purchases for DCA investors and has an intuitive interface perfect for beginners. Their Coinbase One subscription eliminates trading fees entirely for $29.99/month, though this only makes sense for larger investment amounts.

- Cash App: Particularly student-friendly with no minimum purchase amounts and the ability to buy Bitcoin with as little as $1. Perfect for testing DCA strategies before committing larger amounts.

- Swan Bitcoin: Specializes in Bitcoin DCA with competitive fees and educational resources. Their platform is built specifically for long-term Bitcoin accumulation rather than trading.

- Strike: Offers commission-free Bitcoin purchases funded directly from your bank account. Their DCA feature is straightforward and cost-effective for regular purchases.

TuitionHero Tip

Compare fee structures carefully. A 1% fee might seem small, but it can add up over time, reducing investment returns. Some platforms offer fee-free DCA options that can save meaningful money over time.

Common DCA mistakes to avoid

Even a simple strategy like DCA has potential pitfalls that can derail your investment success.

- Stopping during market crashes: The hardest part of DCA is continuing to buy when prices are falling and news headlines are scary. These are often the best times to be buying, but they feel the worst emotionally.

- Increasing purchases during rallies: When Bitcoin hits new all-time highs, resist the urge to double or triple your normal DCA amount. Stick to your plan, or you'll end up buying more at higher prices.

- Choosing too high an amount: Starting with unsustainable investment amounts leads to missed payments and inconsistent DCA execution. Better to invest $25 consistently than $100 sporadically.

- Neglecting security: Leaving your accumulated crypto on exchanges indefinitely increases risk. Consider moving larger amounts to a hardware wallet for long-term storage.

- Ignoring tax implications: Every DCA purchase creates a taxable event when you eventually sell. Keep detailed records of purchase dates, amounts, and prices for tax reporting.

Tax considerations for student crypto investors

Cryptocurrency investments have tax implications that students should understand before starting their DCA strategy.

- Each sale is taxable: When you sell cryptocurrency, you'll owe capital gains taxes on any profits. This applies even to small amounts or partial sales.

- Record-keeping requirements: The IRS requires detailed records of all crypto transactions. Your DCA purchases create multiple "tax lots" with different purchase dates and costs.

- Student tax advantages: Many students fall into lower tax brackets, making long-term capital gains rates (for crypto held over one year) particularly attractive. Current long-term rates for lower incomes can be 0% or 15%.

- Tax software integration: Popular platforms like Coinbase integrate with tax software like TurboTax, simplifying the reporting process for your DCA transactions.

TuitionHero Tip

Keep a simple spreadsheet tracking your DCA purchases, or use portfolio tracking apps like CoinTracker that automatically calculate tax obligations. Starting this habit early saves major headaches later.

Crypto DCA vs. Lump sum investing

Strategy | Best For | Pros | Cons |

|---|---|---|---|

Dollar-Cost Averaging | Students with limited capital | Reduces volatility impact, manageable amounts, less stressful | May miss out on gains during bull runs |

Lump Sum Investing | Investors with large amounts ready to invest | Maximizes time in market, potentially higher returns | Requires market timing, higher risk |

Hybrid Approach | Flexible investors | Combines benefits of both strategies | More complex to execute |

Dos and don'ts of dollar-cost averaging crypto

Do

Start small and stay consistent

Automate your purchases

Focus on established cryptocurrencies initially

Keep detailed records for taxes

Continue buying during market downturns

Don't

Don't invest money you need for tuition or living expenses

Don't check prices obsessively

Don't stop DCA during bear markets

Don't chase trending altcoins with your DCA money

Don't forget about exchange security

Why trust TuitionHero

At TuitionHero, we help you find the best private student loans by comparing top lenders and breaking down eligibility, interest rates, and repayment options. Whether you need additional funding beyond federal aid or a loan without a cosigner, we simplify the process. We also provide expert insights on refinancing, FAFSA assistance, scholarships, and student credit cards to support your financial success.

Frequently asked questions (FAQ)

Start with an amount you can truly afford to lose if the market crashes, typically $25-100 per month for most students. This should be money beyond your emergency fund and essential expenses. You can always increase the amount as your income grows after graduation.

Monthly DCA works well for most students since it aligns with typical income patterns and reduces transaction fees. Weekly DCA can provide slightly better volatility smoothing, but it isn't worth it if the additional fees eat into your returns significantly.

Bitcoin is generally considered the standard choice for beginners due to its market dominance and longer track record. Ethereum can also be a compelling choice but might be slightly more volatile. Avoid spreading your initial DCA across multiple cryptocurrencies until you've built substantial positions in one or two.

Missing occasional purchases won't break your strategy, but consistency is key to DCA's effectiveness. If you miss one, just continue with your next scheduled purchase rather than trying to make up for it with a larger amount.

This depends on your financial goals. Many successful DCA investors continue for years, viewing crypto as a long-term store of value. Consider selling portions when you need money for major life events like graduate school, a house down payment, or starting a business.

Final thoughts

Dollar-cost averaging is a smart way for students to get into crypto without all the usual stress and big upfront costs. Because it's all about regular, consistent contributions instead of trying to time the market, it fits perfectly with student life and budgets.

Just remember, crypto is still pretty wild and speculative. Don't put in more than you can afford to completely lose. Think of it as just one piece of your overall financial plan that also includes emergency savings and other investments down the road.

So, whether you're into Bitcoin, worried about inflation, or just want to get in on the digital economy, DCA offers a solid way to start. And hey, TuitionHero's student loan and financial planning tools can help you balance crypto investing with your other financial goals, making sure your interest in investing doesn't mess with your education.

Source

Author

Derick Rodriguez

Derick Rodriguez is a seasoned editor and digital marketing strategist specializing in demystifying college finance. With over half a decade of experience in the digital realm, Derick has honed a unique skill set that bridges the gap between complex financial concepts and accessible, user-friendly communication. His approach is deeply rooted in leveraging personal experiences and insights to illuminate the nuances of college finance, making it more approachable for students and families.

Editor

Brian Flaherty

Brian is a graduate of the University of Virginia where he earned a B.A. in Economics. After graduation, Brian spent four years working at a wealth management firm advising high-net-worth investors and institutions. During his time there, he passed the rigorous Series 65 exam and rose to a high-level strategy position.

At TuitionHero, we're not just passionate about our work - we take immense pride in it. Our dedicated team of writers diligently follows strict editorial standards, ensuring that every piece of content we publish is accurate, current, and highly valuable. We don't just strive for quality; we aim for excellence.

Related posts

While you're at it, here are some other college finance-related blog posts you might be interested in.

3 minutes read

Where Did Morgan Wallen Go to College? The Unexpected Path of a Country Star

Did Morgan Wallen go to college? See how a baseball injury changed his plans and how students can learn from his journey.

Learn More

5 minutes read

How to Build a Strong Resume for Internships

Wondering how to craft a compelling internship resume that grabs attention? Discover essential strategies to build a standout resume and secure your dream internship.

Learn More

8 minutes read

How to Get Your Student Loans Forgiven

Learn how to erase student loan debt with our top strategies for Public Service Loan Forgiveness, including employer tips and payment plans.

Learn More

Shop and compare student financing options - 100% free!

Always free, always fast

TuitionHero is 100% free to use. Here, you can instantly view and compare multiple top lenders side-by-side.

Won’t affect credit score

Don’t worry – checking your rates with TuitionHero never impacts your credit score!

Safe and secure

We take your information's security seriously. We apply industry best practices to ensure your data is safe.

Finished scrolling? Start saving & find your private student loan rate today

Compare Personalized Rates