![]()

Advertiser Disclosure

Last update: September 23, 2025

7 minutes read

What is Buy Now, Pay Later for Textbooks? The Payment Plan Dividing Students

Wondering if buy now, pay later is worth it for expensive textbooks? We break down the pros, cons, and hidden costs of splitting textbook payments into installments.

By Derick Rodriguez, Associate Editor

Edited by Yerain Abreu, M.S.

Learn more about our editorial standards

By Derick Rodriguez, Associate Editor

Edited by Yerain Abreu, M.S.

Learn more about our editorial standards

Ever stood at the campus bookstore checkout, staring at a $400 textbook bill and feeling your stomach drop?

With textbook prices skyrocketing, more students are turning to buy now, pay later (BNPL) services to split these crushing costs into smaller payments. But is this financial shortcut actually helping or creating bigger problems down the road?

Key takeaways

- BNPL services like Klarna, Afterpay, and Affirm let you split textbook costs into smaller payments, usually over 6-12 weeks

- These services can help with cash flow but may encourage overspending on unnecessary materials

- Students should consider alternatives like textbook rentals, used books, or digital editions before committing to payment plans

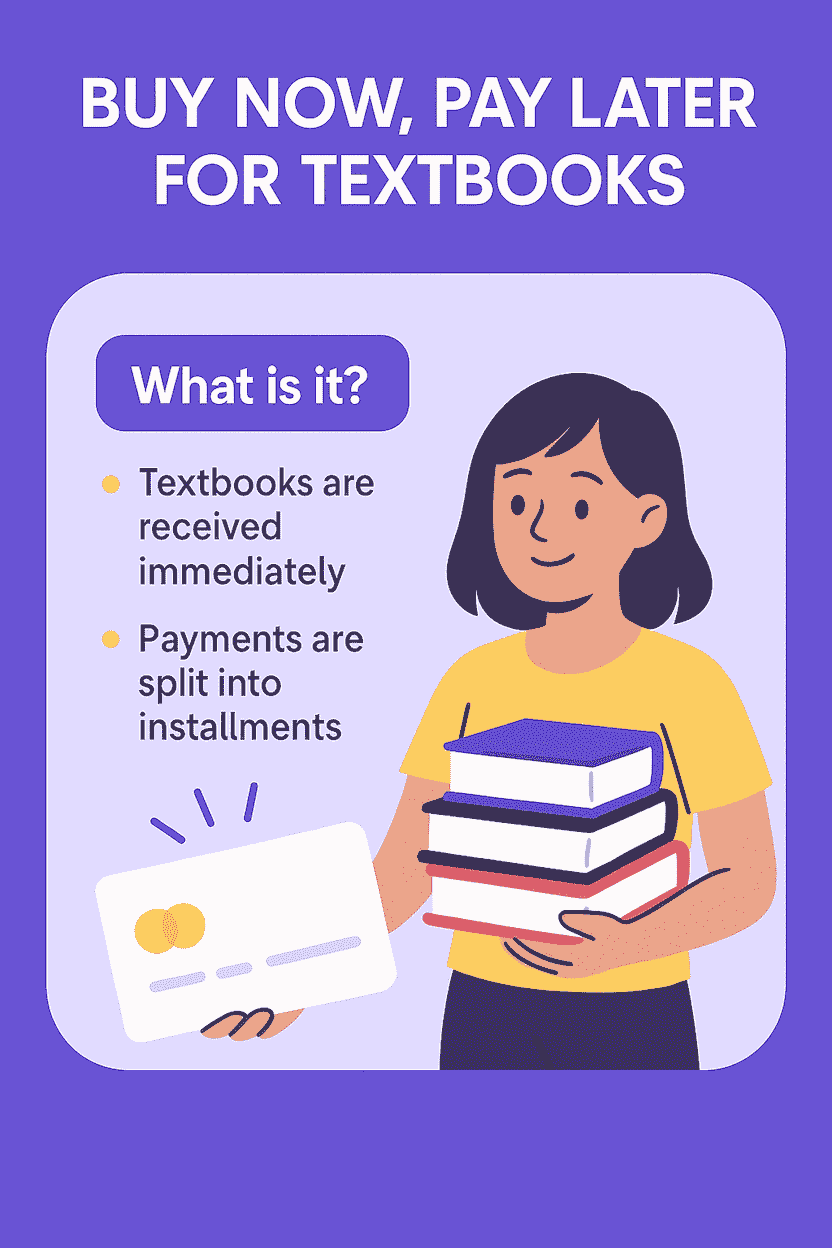

What is buy now, pay later?

Buy now, pay later (BNPL) is a payment method that splits your purchase into smaller installments over time. Instead of paying $300 upfront for that organic chemistry textbook, you might pay $75 every two weeks for eight weeks.

Most BNPL services split purchases into four equal payments over 6-8 weeks. Some offer longer terms with 6-12 monthly payments, though these sometimes include interest charges. Popular BNPL providers include:

- Klarna

- Afterpay

- Affirm

- Zip

These services typically don't require a hard credit check for approval, making them accessible to students with limited credit history.

How does buy now, pay later work for textbooks?

BNPL services partner with college bookstores and online textbook retailers to offer payment splitting at checkout.

The process is surprisingly simple:

- You choose BNPL at checkout

- Get approved in seconds (usually with just a soft credit check)

- Receive your books immediately

The catch? You're locked into a payment schedule, whether your financial situation changes or not.

Miss your part-time job? You still owe those payments. Financial aid delayed? Payments continue as scheduled.

TuitionHero Tip

Always read the fine print before agreeing to any payment plan. What seems like "0% interest" might come with hefty late fees that quickly add up.

Which retailers offer BNPL for textbooks?

Major textbook sellers have jumped on the BNPL bandwagon.

- Amazon offers payment plans through Affirm for textbook purchases over $50.

- Chegg partners with multiple BNPL providers, letting you split both textbook purchases and rental fees.

- Klarna, Afterpay, or Zip are now accepted at checkout at many campus bookstores.

- VitalSource, the digital textbook giant, recently added BNPL options for its e-textbook purchases.

- Even smaller, independent bookstores are adding these services to compete with larger retailers.

The variety of options means you can likely find a BNPL service for whatever textbook source you prefer. But having more choices doesn't automatically make it the right financial decision.

Compare private student loans now

TuitionHero simplifies your student loan decision, with multiple top loans side-by-side.

Compare Rates

What are the real costs of BNPL for textbooks?

Here's where things get tricky. Most BNPL services advertise "0% interest" and "no fees", but that's only if everything goes perfectly.

Miss a payment? You could face late fees ranging from $7 to $25 per occurrence.

Some services also charge processing fees, especially for longer payment terms. Affirm, for example, might charge interest rates between 0-36% APR, depending on your creditworthiness and the payment term you choose.

There's also an opportunity cost to consider. That $300 textbook split over two months might prevent you from taking advantage of better deals. Used textbook prices often drop significantly after the first few weeks of the semester, but you're locked into paying full price.

TuitionHero Tip

Calculate the total cost, including any potential fees, before choosing BNPL. Sometimes paying upfront with a student discount saves more money than splitting payments.

Who should consider BNPL for textbooks?

BNPL makes the most sense for students facing temporary cash flow issues. Splitting textbook costs can provide breathing room if you’re:

- Waiting for financial aid to disburse

- Expecting a paycheck, or

- Dealing with an emergency expense

Students with predictable income from part-time jobs or internships often manage BNPL payments successfully. The key is having confidence that you can make every payment on time.

However, BNPL isn't ideal for everyone. You should think twice about using BNPL if you’re:

- A student already struggling with debt

- Don’t have a steady income

- Are prone to impulse purchases

Are there better alternatives to BNPL for textbooks?

Before committing to a payment plan, explore these money-saving options:

- Textbook rentals from Chegg, Amazon, or your campus library can cut costs by 50-80%.

- Used textbooks from sites like AbeBooks or fellow students offer significant savings.

- Digital editions often cost less than physical books and can't be "lost" or damaged.

- Many professors put textbooks on reserve in the library.

- Open Educational Resources (OER) provide free textbook alternatives for many subjects.

- Some schools offer textbook voucher programs for students with financial need.

TuitionHero Tip

Check if your school offers textbook lending programs or emergency funding for educational materials before turning to payment plans.

What students are saying about BNPL for textbooks

Student opinions on BNPL for textbooks are deeply divided. Supporters appreciate the flexibility, especially when financial aid is delayed or when facing unexpected course requirements.

"I needed my calculus textbook immediately, but my refund check wasn't coming for three weeks," explains Teresa, a college sophomore. "BNPL let me get the book and stay caught up in class."

Critics worry about the spending habits BNPL encourages. "It made buying the $400 textbook 'bundle' feel affordable, even though I only needed the basic book," admits Marcus, a junior business major. "I ended up paying for access codes I never used."

Financial counselors at many colleges report seeing students struggle with multiple BNPL payments across different purchases, creating a cycle of payment obligations that's hard to escape.

Pros | Cons |

|---|---|

Immediate access to required materials | Potential for overspending |

No upfront payment burden | Late fees if payments are missed |

Usually no interest if paid on time | Less flexibility than other options |

Quick approval process | Can create payment fatigue |

Tips for using BNPL responsibly for textbooks

If you decide BNPL is right for your situation, follow these guidelines to avoid financial trouble:

- Set up automatic payments to avoid late fees.

- Keep track of all your BNPL obligations in a calendar or app.

- Only use BNPL for textbooks you absolutely need, not "nice to have" study materials.

- Budget for the full payment schedule before making the purchase.

If you can't afford the payments comfortably, the textbook is probably outside your budget, regardless of the payment plan.

Consider setting aside money from each payment to build an emergency fund for future textbook purchases.

Why trust TuitionHero

At TuitionHero, we help you find the best private student loans by comparing top lenders and breaking down eligibility, interest rates, and repayment options. Whether you need additional funding beyond federal aid or a loan without a cosigner, we simplify the process. We also provide expert insights on refinancing, FAFSA assistance, scholarships, and student credit cards to support your financial success.

Frequently asked questions (FAQ)

Most BNPL services only perform soft credit checks for approval, which don't impact your credit score. However, some providers like Affirm report payment history to credit bureaus, which can affect your score positively or negatively.

As of 2025, major credit scoring companies are starting to include BNPL payment history into credit scores.

Return policies vary by retailer and BNPL provider. You're typically still responsible for payments even if you return the item, though some services pause payments during the return process.

You'll likely face late fees immediately. Some services offer grace periods or payment rescheduling, but repeated missed payments could result in your account being sent to collections.

Each service sets its own limits based on your payment history and creditworthiness. Having multiple BNPL obligations can impact your approval for new purchases.

Most services allow early payoff without penalties. This can be a good strategy if you receive financial aid or other funds before your payment schedule ends.

Final thoughts

BNPL for textbooks works well for some students and poorly for others. If you're disciplined with payments and need immediate access to course materials, it can provide valuable flexibility. But if you're already struggling financially or tend toward impulse purchases, these services might create more problems than they solve.

TuitionHero offers resources to help you find affordable textbook options and manage education expenses. Before committing to any payment plan, explore all your alternatives first.

Source

Author

Derick Rodriguez

Derick Rodriguez is a seasoned editor and digital marketing strategist specializing in demystifying college finance. With over half a decade of experience in the digital realm, Derick has honed a unique skill set that bridges the gap between complex financial concepts and accessible, user-friendly communication. His approach is deeply rooted in leveraging personal experiences and insights to illuminate the nuances of college finance, making it more approachable for students and families.

Editor

Yerain Abreu

Yerain Abreu is a Content Strategist with over 7 years of experience. He earned a Master's degree in digital marketing from Zicklin School of Business. He focuses on college finance, a niche carved out of his journey through the complexities of academic finance. These firsthand experiences provide him with a unique perspective, enabling him to create content that's informative and relatable to students and their families grappling with the intricacies of college financing.

At TuitionHero, we're not just passionate about our work - we take immense pride in it. Our dedicated team of writers diligently follows strict editorial standards, ensuring that every piece of content we publish is accurate, current, and highly valuable. We don't just strive for quality; we aim for excellence.

Related posts

While you're at it, here are some other college finance-related blog posts you might be interested in.

3 minutes read

Where Did Morgan Wallen Go to College? The Unexpected Path of a Country Star

Did Morgan Wallen go to college? See how a baseball injury changed his plans and how students can learn from his journey.

Learn More

5 minutes read

How to Build a Strong Resume for Internships

Wondering how to craft a compelling internship resume that grabs attention? Discover essential strategies to build a standout resume and secure your dream internship.

Learn More

8 minutes read

How to Get Your Student Loans Forgiven

Learn how to erase student loan debt with our top strategies for Public Service Loan Forgiveness, including employer tips and payment plans.

Learn More

Shop and compare student financing options - 100% free!

Always free, always fast

TuitionHero is 100% free to use. Here, you can instantly view and compare multiple top lenders side-by-side.

Won’t affect credit score

Don’t worry – checking your rates with TuitionHero never impacts your credit score!

Safe and secure

We take your information's security seriously. We apply industry best practices to ensure your data is safe.

Finished scrolling? Start saving & find your private student loan rate today

Compare Personalized Rates